Maximize Your Retirement Savings 2026: IRA & 401(k) Contributions

Retirement planning is not merely a financial exercise; it’s a profound commitment to your future self, ensuring that your golden years are filled with comfort, security, and the freedom to pursue your passions without financial constraint. As we look ahead to 2026, understanding how to maximize retirement savings becomes paramount. The landscape of retirement accounts, tax laws, and investment opportunities is constantly evolving, making it essential to stay informed and strategic. This comprehensive guide will delve into the intricacies of maximizing your contributions to IRAs and 401(k)s, exploring the pivotal role these vehicles play in accumulating wealth and significantly reducing your tax burden.

For many, the idea of retirement feels distant, a far-off dream. However, the sooner you begin to strategize and contribute, the more powerful the effect of compounding interest becomes. This article aims to demystify the process, providing actionable insights and expert advice to help you navigate the complexities of retirement planning for 2026. We’ll cover everything from understanding contribution limits and eligibility criteria to choosing between traditional and Roth options, and even advanced strategies for those who wish to go above and beyond the standard contributions. Our goal is to empower you to make informed decisions that will lead to a robust and fulfilling retirement.

The Foundation of Financial Security: Understanding IRAs and 401(k)s

Before we dive into the specifics of maximizing your contributions, it’s crucial to have a solid understanding of the primary retirement vehicles available: Individual Retirement Arrangements (IRAs) and 401(k)s. While both serve the ultimate purpose of helping you save for retirement, they differ significantly in their structure, contribution limits, tax implications, and employer involvement.

Individual Retirement Arrangements (IRAs)

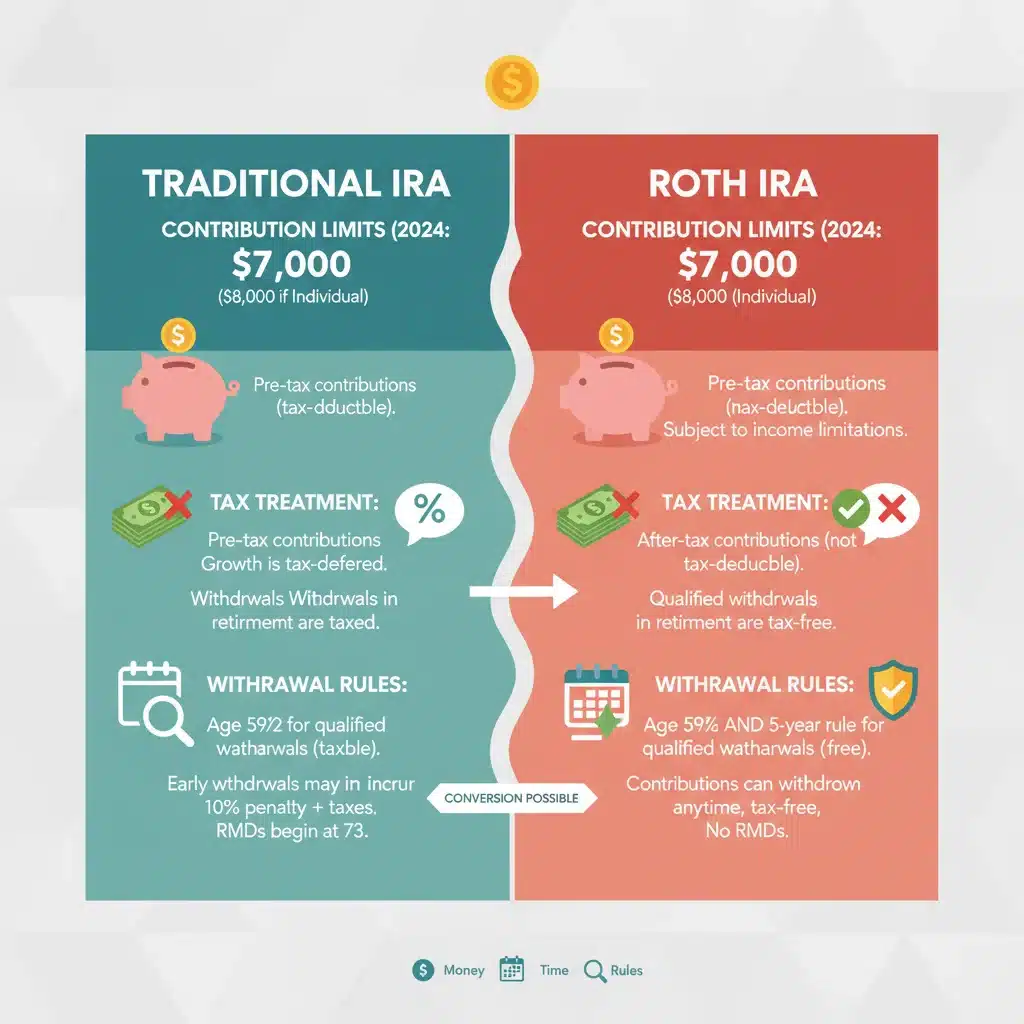

IRAs are personal savings plans that offer tax advantages for retirement savings. They are not tied to an employer, giving individuals more control over their investments. There are primarily two types of IRAs that most people utilize:

- Traditional IRA: Contributions to a Traditional IRA are often tax-deductible in the year they are made, which can lower your taxable income. Earnings grow tax-deferred, meaning you don’t pay taxes on them until you withdraw the money in retirement. Withdrawals in retirement are taxed as ordinary income.

- Roth IRA: Contributions to a Roth IRA are made with after-tax dollars, meaning they are not tax-deductible. However, the significant advantage of a Roth IRA is that qualified withdrawals in retirement are completely tax-free. This includes both your contributions and all the earnings they’ve generated over the years.

The choice between a Traditional and Roth IRA often depends on your current income level, your expected income in retirement, and your tax philosophy. If you anticipate being in a higher tax bracket in retirement, a Roth IRA might be more advantageous. Conversely, if you expect to be in a lower tax bracket in retirement, a Traditional IRA could offer more immediate tax benefits.

401(k) Plans

A 401(k) is an employer-sponsored retirement plan, meaning it’s offered through your workplace. These plans allow employees to contribute a portion of their pre-tax salary directly from their paycheck, automatically reducing their taxable income. Like Traditional IRAs, contributions and earnings grow tax-deferred until retirement.

Key features of 401(k)s include:

- Higher Contribution Limits: 401(k)s generally allow for much higher annual contributions than IRAs, making them powerful tools for maximizing retirement savings.

- Employer Matching Contributions: One of the most attractive features of a 401(k) is the potential for employer matching contributions. Many employers will match a percentage of your contributions up to a certain limit, essentially offering free money towards your retirement. Failing to contribute enough to get the full employer match is like turning down a pay raise.

- Loan Options: Some 401(k) plans allow you to borrow against your account balance, though this should generally be considered a last resort.

- Roth 401(k) Option: Similar to a Roth IRA, many 401(k) plans now offer a Roth option, allowing after-tax contributions and tax-free withdrawals in retirement.

Understanding the nuances of these accounts is the first step toward building a robust retirement plan. Now, let’s explore how to leverage them to maximize your savings in 2026.

2026 Contribution Limits: What to Expect and How to Plan

Contribution limits for IRAs and 401(k)s are adjusted periodically by the IRS to account for inflation and other economic factors. While the exact figures for 2026 are typically announced later in the preceding year, we can project based on historical trends and current economic indicators. It’s crucial to stay updated on these figures as they are the cornerstone of your maximization strategy.

Projected IRA Contribution Limits for 2026

For 2024, the IRA contribution limit is $7,000, with an additional catch-up contribution of $1,000 for those aged 50 and over. Based on historical adjustments, it’s reasonable to anticipate a slight increase for 2026. For illustrative purposes, let’s assume a potential increase to approximately $7,500 for those under 50 and $8,500 for those 50 and over (including catch-up). These numbers are hypothetical but serve to demonstrate the potential for increased savings.

Regardless of the exact figure, the strategy remains the same: aim to contribute the maximum allowed. Even if you can’t contribute the full amount at once, setting up automated contributions throughout the year can make it more manageable. For example, dividing the annual limit by 12 and setting up a monthly direct deposit can help you consistently hit your target.

Projected 401(k) Contribution Limits for 2026

The 401(k) contribution limits are typically much higher than those for IRAs. For 2024, the limit is $23,000, with an additional catch-up contribution of $7,500 for those aged 50 and over. Given historical trends, we could see the regular contribution limit for 2026 approach $24,000 or $24,500, with the catch-up contribution potentially rising to $8,000. This means individuals aged 50 and over could potentially contribute over $32,000 to their 401(k) in 2026.

Hitting the maximum 401(k) contribution requires a significant commitment, but the long-term benefits are immense. If your employer offers a match, prioritize contributing at least enough to receive the full match. This is free money that significantly boosts your retirement savings.

Strategies to Maximize Retirement Savings in 2026

Now that we understand the basics and projected limits, let’s explore practical strategies to maximize retirement savings in 2026. These strategies involve a combination of disciplined saving, smart account utilization, and strategic tax planning.

1. Automate Your Contributions

The easiest way to ensure you’re consistently saving is to automate the process. Set up automatic transfers from your checking account to your IRA, or adjust your 401(k) contributions directly from your paycheck. This ‘set it and forget it’ approach removes the temptation to spend the money elsewhere and ensures you’re always making progress towards your goals.

2. Prioritize Employer Match in Your 401(k)

As mentioned, if your employer offers a 401(k) match, contributing enough to receive the full match should be your absolute top priority. It’s an immediate, guaranteed return on your investment that you won’t find anywhere else. Think of it as an instant boost to your retirement fund.

3. Max Out Your IRA (Traditional or Roth)

Once you’ve secured your employer match, the next step is to maximize your IRA contributions. Whether you choose a Traditional or Roth IRA depends on your individual circumstances and tax outlook. If you’re eligible for both, consider diversifying your tax treatment by contributing to both a pre-tax (401(k) or Traditional IRA) and an after-tax (Roth IRA) account.

4. Max Out Your 401(k) Beyond the Match

After maximizing your IRA, if you still have disposable income, direct it towards maxing out your 401(k) contributions up to the annual limit. The higher limits in 401(k)s make them incredibly powerful for aggressive savers. This is particularly beneficial if you have access to a Roth 401(k) option, allowing you to contribute a substantial amount of after-tax money that grows tax-free.

5. Utilize Catch-Up Contributions (Age 50 and Over)

For those aged 50 and over, the IRS allows for additional ‘catch-up’ contributions to both IRAs and 401(k)s. These extra contributions are a golden opportunity to supercharge your savings in the years leading up to retirement. If you’re in this age group, make every effort to take advantage of these higher limits.

6. Consider a Health Savings Account (HSA) – The Triple Tax Advantage

While not strictly a retirement account, a Health Savings Account (HSA) is often referred to as the ‘triple tax advantage’ account and can serve as a powerful supplementary retirement savings vehicle. Contributions are tax-deductible, earnings grow tax-free, and qualified withdrawals for medical expenses are also tax-free. If you’re enrolled in a high-deductible health plan (HDHP), an HSA is an excellent tool to consider for both current healthcare costs and future medical expenses in retirement.

7. Backdoor Roth IRA Strategy

If your income exceeds the limits for directly contributing to a Roth IRA, you might still be able to contribute through a ‘backdoor Roth IRA’ strategy. This involves contributing to a non-deductible Traditional IRA and then converting it to a Roth IRA. While there are no income limits for conversions, it’s a strategy that requires careful consideration of the ‘pro-rata rule’ if you have existing pre-tax IRA balances. Consulting a financial advisor for this strategy is highly recommended.

8. Mega Backdoor Roth Strategy (if available)

For those with a 401(k) that allows after-tax contributions and in-service rollovers to a Roth IRA, the ‘mega backdoor Roth’ can be an extremely powerful way to contribute significantly more after-tax money into a Roth vehicle. This strategy leverages the total 401(k) limit (employee contributions + employer contributions + after-tax contributions) which can be much higher than the standard employee contribution limit. Again, this is an advanced strategy that requires your 401(k) plan to support it and often benefits from professional guidance.

The Power of Tax Savings and Compounding

Maximizing your retirement contributions isn’t just about accumulating a larger nest egg; it’s also about leveraging significant tax advantages and the unparalleled power of compounding interest.

Tax Advantages

- Immediate Tax Deductions: Contributions to a Traditional IRA and a traditional 401(k) reduce your taxable income in the year you make them, potentially lowering your current tax bill.

- Tax-Deferred Growth: Earnings within Traditional IRAs and 401(k)s grow without being taxed until withdrawal in retirement. This allows your investments to compound more aggressively without annual tax drag.

- Tax-Free Withdrawals: Qualified withdrawals from Roth IRAs and Roth 401(k)s are completely tax-free in retirement, which can be a huge advantage, especially if you expect to be in a higher tax bracket later in life.

Compounding Interest

Compounding interest is often called the ‘eighth wonder of the world.’ It’s the process where the interest you earn also starts earning interest. The longer your money is invested, the more powerful compounding becomes. By consistently contributing the maximum to your retirement accounts, you give your money more time and more capital to grow exponentially.

Imagine contributing $23,000 to your 401(k) every year for 30 years. If your investments grow at an average annual rate of 7%, you would accumulate a substantial sum, far exceeding the total amount you contributed. The earlier you start and the more you contribute, the greater the impact of compounding on your final retirement balance.

Navigating Investment Choices Within Your Retirement Accounts

Contributing the maximum is only half the battle; the other half is making smart investment choices within your IRA and 401(k). The specific investment options available will vary depending on your account provider (for IRAs) or your employer’s plan (for 401(k)s).

Diversification is Key

Don’t put all your eggs in one basket. Diversify your investments across different asset classes, such as stocks, bonds, and potentially real estate or other alternative investments. This helps mitigate risk and can lead to more consistent returns over the long term.

Consider Your Risk Tolerance and Time Horizon

Your investment strategy should align with your personal risk tolerance and how many years you have until retirement. Younger investors with a long time horizon can generally afford to take on more risk with a higher allocation to stocks, which historically offer higher returns. As you approach retirement, it’s generally advisable to shift towards more conservative investments to protect your accumulated capital.

Utilize Target-Date Funds

For those who prefer a hands-off approach, target-date funds can be an excellent option. These funds automatically adjust their asset allocation over time, becoming more conservative as you approach the target retirement date. They offer built-in diversification and rebalancing.

Regularly Review and Rebalance

It’s important to periodically review your investment portfolio (at least annually) to ensure it still aligns with your goals and risk tolerance. Market fluctuations can cause your asset allocation to drift, so rebalancing your portfolio back to your desired percentages is crucial.

Common Pitfalls to Avoid in Retirement Planning

While maximizing contributions is vital, being aware of common mistakes can prevent setbacks in your retirement journey.

1. Not Starting Early Enough

The biggest mistake is delaying your retirement savings. The power of compounding means that every year you delay, you lose out on significant potential growth. Start saving, even a small amount, as soon as possible.

2. Not Taking Advantage of Employer Match

As emphasized earlier, leaving employer match money on the table is a missed opportunity for free money. Make sure you contribute at least enough to get the full match.

3. Being Too Conservative (or Too Aggressive)

While balancing risk is important, being too conservative, especially early on, can lead to your money not growing enough to keep pace with inflation. Conversely, being too aggressive close to retirement can expose you to unnecessary market risk. Find a balance that suits your individual profile.

4. Forgetting About Inflation

The cost of living will likely be higher in the future. Ensure your retirement savings strategy accounts for inflation so that your accumulated wealth maintains its purchasing power.

5. Not Having a Plan

Winging it for retirement is a recipe for disaster. Develop a clear plan, set specific goals, and regularly review your progress. Consider working with a financial advisor to create a personalized retirement strategy.

6. Overlooking Healthcare Costs

Healthcare expenses can be a significant burden in retirement. Factor these potential costs into your planning, and consider utilizing an HSA if eligible.

The Role of a Financial Advisor

While this guide provides a wealth of information, navigating the complexities of retirement planning can still be daunting. A qualified financial advisor can offer personalized guidance tailored to your specific situation, goals, and risk tolerance. They can help you:

- Determine appropriate contribution levels to maximize retirement savings.

- Choose the right mix of Traditional and Roth accounts.

- Develop an optimal investment strategy within your accounts.

- Navigate advanced strategies like backdoor Roth or mega backdoor Roth.

- Plan for other financial goals alongside retirement.

- Stay updated on changing tax laws and contribution limits for 2026 and beyond.

Think of a financial advisor as a partner in your financial journey, helping you make informed decisions and stay on track to achieve a secure and comfortable retirement.

Conclusion: Your Path to a Secure Retirement in 2026 and Beyond

Maximizing your retirement savings in 2026 by fully utilizing your IRA and 401(k) contributions is one of the most impactful financial decisions you can make. It’s a proactive step towards securing your financial independence and ensuring a comfortable future. By understanding the different account types, staying informed about contribution limits, and implementing strategic saving and investment practices, you can significantly enhance your retirement outlook.

Remember, consistency is key. Automate your savings, prioritize employer matches, and make every effort to contribute the maximum allowed to these powerful tax-advantaged accounts. The sooner you start and the more diligently you save, the more time compounding interest has to work its magic, transforming your consistent contributions into a substantial nest egg.

Start planning today for 2026. Review your current contributions, assess your financial capacity, and make the necessary adjustments to ensure you are on the fast track to maximizing your retirement savings. Your future self will thank you for the foresight and discipline you demonstrate today.

2026: Limits, Strategies & Future Growth")

for 2025: New $23,000 Limit Guide")

Contributions in 2026: A US Guide")

")