Navigating Medicare Part B Premiums 2026: Your Essential Guide

Navigating Medicare Part B Premiums for 2026: What You Need to Know Now

As we move closer to 2026, understanding the intricacies of Medicare, especially the upcoming changes to Medicare Part B Premiums, becomes increasingly vital for millions of Americans. Medicare is a lifeline for seniors and individuals with certain disabilities, providing essential health coverage. However, the costs associated with Medicare, particularly Part B, can fluctuate annually, making proactive planning indispensable. This comprehensive guide aims to demystify the projected changes for 2026, offering insights into what beneficiaries can expect and how they can best prepare to manage their healthcare expenses.

The Centers for Medicare & Medicaid Services (CMS) typically announces the official Medicare Part B premium amounts in the fall preceding the new year. While we don’t have the final figures for 2026 yet, we can analyze historical trends, economic indicators, and legislative considerations to provide an informed outlook. Being prepared means understanding not just the numbers, but also the factors that influence these premiums, such as the Income-Related Monthly Adjustment Amount (IRMAA), Medicare’s financial health, and the broader economic landscape.

For many, the annual adjustment of Medicare Part B Premiums is a significant financial consideration. Staying informed and developing a strategic approach to healthcare budgeting can help alleviate potential stress and ensure continued access to necessary medical services. Let’s delve into the details and equip you with the knowledge to navigate these changes effectively.

Understanding Medicare Part B: The Basics

Before we explore the future, it’s crucial to have a solid grasp of what Medicare Part B covers and how its premiums are structured. Medicare Part B, also known as medical insurance, covers medically necessary services and supplies, including doctor’s visits, outpatient care, preventive services, and some home health care. It’s a fundamental component of Original Medicare, working in conjunction with Part A (hospital insurance).

What Does Medicare Part B Cover?

- Doctor’s Services: This includes visits to your primary care physician and specialists.

- Outpatient Care: Services received at a hospital outpatient department, such as emergency room visits, observation stays, and some surgeries.

- Preventive Services: Screenings, vaccines, and annual wellness visits designed to keep you healthy and detect problems early.

- Medical Equipment: Durable medical equipment (DME) like wheelchairs, walkers, and oxygen equipment.

- Mental Health Services: Outpatient mental health care, including therapy and counseling.

- Laboratory Tests and X-rays: Diagnostic services crucial for identifying and monitoring health conditions.

It’s important to remember that Medicare Part B typically covers 80% of the Medicare-approved amount for most services after you meet your annual deductible. The remaining 20% is your responsibility, unless you have supplemental insurance (like Medigap) or a Medicare Advantage plan that covers these costs.

How Are Medicare Part B Premiums Determined?

The standard Medicare Part B Premiums are set annually by the federal government. Several factors contribute to this determination:

- Cost of Healthcare Services: The overall expenditure on doctor’s services, outpatient care, and medical supplies directly impacts premium costs. Advances in medical technology and new treatments, while beneficial, can drive up expenses.

- Medicare’s Financial Health: The solvency of the Medicare trust funds plays a significant role. When expenditures exceed revenues, adjustments are often made to premiums and deductibles.

- Economic Factors: Inflation, wage growth, and the broader economic climate can influence healthcare costs and, consequently, Medicare premiums.

- Legislative Changes: Congress can pass laws that affect Medicare funding, benefit structures, and premium calculations.

- The ‘Hold Harmless’ Provision: This provision often protects many Medicare beneficiaries from significant premium increases if their Social Security cost-of-living adjustment (COLA) is not sufficient to cover the rise in premiums. However, this protection doesn’t apply to all beneficiaries, especially those subject to IRMAA.

Understanding these foundational elements is key to appreciating the potential shifts in Medicare Part B Premiums for 2026.

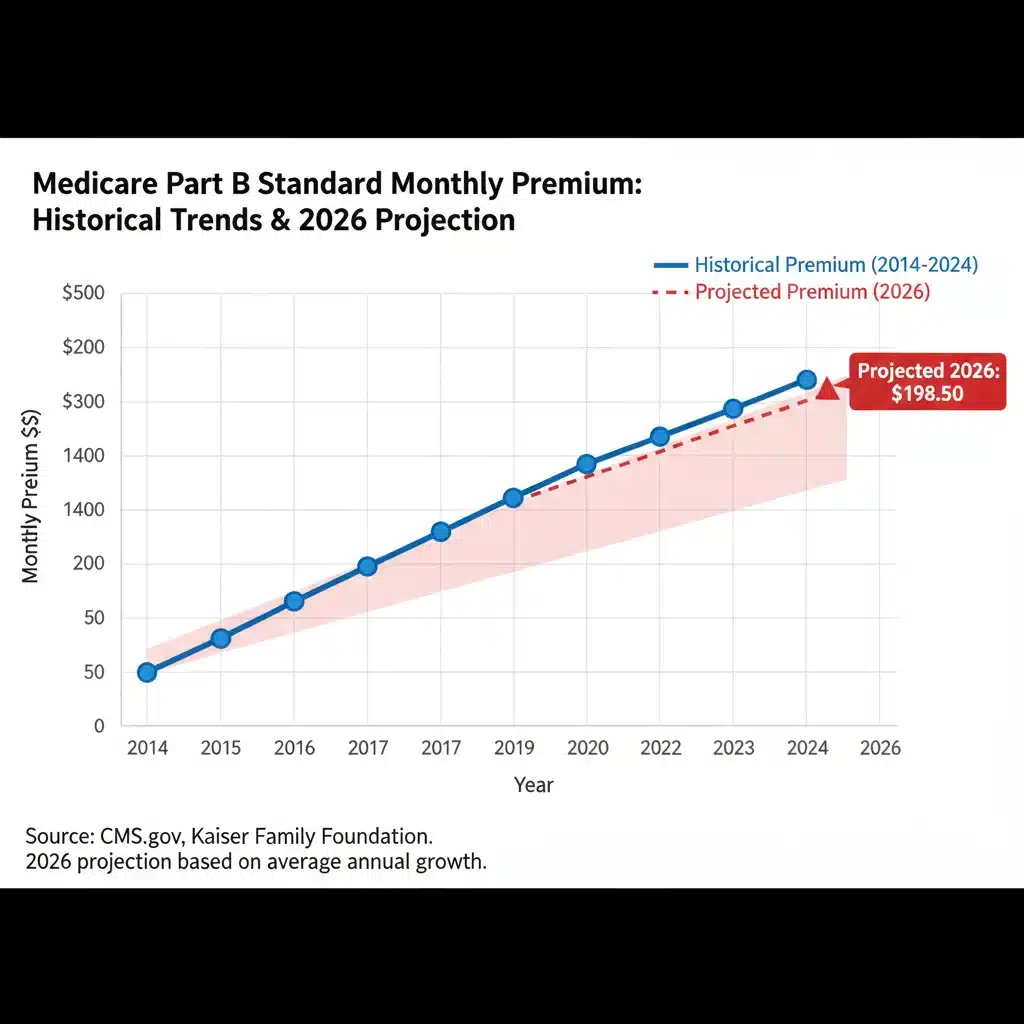

Projected Changes for Medicare Part B Premiums in 2026

While specific figures for 2026 are not yet available, we can make educated projections based on current trends and expert analyses. Historically, Medicare Part B Premiums have seen gradual increases, with occasional larger jumps due to specific legislative or economic events. The trajectory of healthcare costs, particularly for prescription drugs and specialized medical procedures, remains a primary driver.

Factors Influencing the 2026 Outlook

- Inflationary Pressures: Persistent inflation across the economy can impact the cost of medical services, supplies, and labor, leading to higher expenditures for Medicare.

- Healthcare Utilization: Changes in how beneficiaries use healthcare services, including an aging population’s increased need for care, can affect overall program costs.

- Prescription Drug Costs: The rising cost of new and existing prescription drugs continues to be a significant concern for Medicare’s budget, potentially influencing Part B premiums.

- Medicare Trust Fund Status: The annual report on the financial status of the Medicare trust funds provides crucial insights. If the trust funds face solvency challenges, premium adjustments might be necessary to ensure the program’s long-term viability.

- Potential Legislative Actions: Any new healthcare legislation passed by Congress could have direct implications for Medicare funding and premium calculations.

Given these factors, it is reasonable to anticipate a moderate increase in the standard Medicare Part B Premiums for 2026. While the ‘hold harmless’ provision offers some protection, many beneficiaries, particularly those with higher incomes, will likely see their premiums rise. It’s essential to monitor official announcements from CMS in late 2025 for the definitive rates.

The Impact of Income: Understanding IRMAA for 2026

One of the most significant factors affecting individual Medicare Part B Premiums is the Income-Related Monthly Adjustment Amount (IRMAA). IRMAA means that if your income is above a certain threshold, you will pay a higher Part B premium. This adjustment applies to approximately 5-6% of Medicare beneficiaries annually.

How IRMAA Works

IRMAA is based on your Modified Adjusted Gross Income (MAGI) from two years prior. So, for 2026 Medicare Part B Premiums, the Social Security Administration (SSA) will typically look at your 2024 tax return. MAGI includes your adjusted gross income plus certain tax-exempt interest income.

The IRMAA thresholds are adjusted annually for inflation. If your MAGI exceeds these thresholds, you will fall into one of several income brackets, each corresponding to a higher Part B premium. These adjustments are not trivial; they can significantly increase your monthly healthcare costs.

Projected IRMAA Brackets for 2026

While the exact IRMAA brackets for 2026 will be released later, we can anticipate their structure will be similar to previous years, with inflation adjustments. For reference, here’s a general idea of how IRMAA tiers typically operate (note: these are illustrative and not the official 2026 figures):

| Tax Filing Status | Modified Adjusted Gross Income (MAGI) | IRMAA Surcharge |

|---|---|---|

| Individual | Up to X | Standard Premium |

| Individual | X to Y | Tier 1 Surcharge |

| Individual | Y to Z | Tier 2 Surcharge |

| Married Filing Jointly | Up to A | Standard Premium |

| Married Filing Jointly | A to B | Tier 1 Surcharge |

| …and so on for higher tiers | … | … |

It’s crucial for those nearing or in retirement to understand how their income, including Social Security benefits, pension income, withdrawals from retirement accounts (like 401(k)s and IRAs), capital gains, and rental income, can impact their MAGI and, consequently, their Medicare Part B Premiums.

Appealing an IRMAA Decision

If your income has significantly decreased since the tax year used for the IRMAA determination (e.g., due to retirement, divorce, or a major life event), you may be able to appeal the decision. You would need to contact the Social Security Administration (SSA) and provide documentation of the life-changing event and your current income. This is a crucial avenue for managing your Medicare Part B Premiums if your financial situation has altered.

Strategies for Managing Medicare Part B Costs in 2026

With the understanding that Medicare Part B Premiums are likely to increase, proactive planning becomes paramount. Here are several strategies beneficiaries can employ to manage their healthcare costs effectively in 2026 and beyond:

1. Proactive Income Planning

Since IRMAA is based on income from two years prior, you have a window to plan. If you anticipate a significant income event (e.g., selling a business, large Roth conversion) in 2024, consider its potential impact on your 2026 Medicare Part B Premiums. Strategies include:

- Managing Retirement Account Withdrawals: Be strategic about when and how much you withdraw from traditional IRAs and 401(k)s. Consider Roth conversions in years with lower income to reduce future Required Minimum Distributions (RMDs) from traditional accounts, which count towards MAGI.

- Tax-Efficient Investing: Utilize tax-advantaged accounts like Roth IRAs and HSAs, as qualified withdrawals from these accounts do not count towards MAGI for IRMAA purposes.

- Delaying Social Security (if applicable): For some, delaying Social Security benefits can temporarily keep MAGI lower, though this is a complex decision with other financial implications.

- Capital Gains Management: If you have investments with significant capital gains, plan their sale strategically across multiple tax years to avoid pushing your MAGI into a higher IRMAA bracket.

2. Explore Medicare Advantage Plans (Part C)

Medicare Advantage plans are offered by private companies approved by Medicare. These plans must cover all the services that Original Medicare (Parts A and B) covers, and often include additional benefits like prescription drug coverage (Part D), dental, vision, and hearing. Many Medicare Advantage plans have premiums as low as $0 (though you still pay your Part B premium) and may offer lower out-of-pocket costs for certain services compared to Original Medicare.

If managing your Medicare Part B Premiums and other out-of-pocket expenses is a priority, exploring Medicare Advantage options during the Annual Enrollment Period (AEP) in the fall of 2025 could be beneficial. Compare plans carefully, considering their network restrictions, co-pays, and maximum out-of-pocket limits.

3. Consider Medigap (Medicare Supplement Insurance)

Medigap policies help cover the ‘gaps’ in Original Medicare, such as deductibles, co-payments, and co-insurance. While you pay a separate premium for Medigap, it can significantly reduce your out-of-pocket costs for services covered by Part A and Part B. If you prefer the flexibility of Original Medicare and want predictable out-of-pocket expenses, a Medigap policy might be a good fit. However, Medigap plans do not cover prescription drugs; you would need a separate Part D plan.

4. Review Prescription Drug Coverage (Part D)

While not directly tied to Medicare Part B Premiums, prescription drug costs can be a major healthcare expense. Review your Part D plan annually during the AEP to ensure it still meets your needs, especially if your medications have changed. Similar to Part B, Part D premiums can also be subject to an IRMAA surcharge if your income exceeds certain thresholds.

5. Utilize Preventive Services

Medicare Part B covers a wide range of preventive services, often at no additional cost if you see a Medicare-approved provider. Taking advantage of annual wellness visits, screenings, and vaccinations can help detect health issues early, potentially preventing more serious and costly conditions down the line. This proactive approach to health management can indirectly help control your overall healthcare spending.

6. Seek Professional Financial Advice

Navigating Medicare and its associated costs can be complex. Consulting with a financial advisor who specializes in retirement planning and Medicare can provide personalized strategies. They can help you analyze your income, identify potential IRMAA triggers, and recommend tax-efficient strategies to manage your wealth in a way that minimizes your Medicare Part B Premiums.

The Broader Economic and Healthcare Landscape

The determination of Medicare Part B Premiums for 2026 doesn’t happen in a vacuum. It’s influenced by a multifaceted array of economic and healthcare factors that are constantly evolving. Understanding these broader dynamics can provide context to the premium adjustments we anticipate.

Healthcare Spending Trends

National healthcare spending continues to rise, driven by factors such as an aging population, the prevalence of chronic diseases, the development of new and often expensive medical technologies and treatments, and the cost of prescription drugs. When overall healthcare costs increase, it places upward pressure on Medicare’s expenditures, which can then translate to higher premiums for beneficiaries. The COVID-19 pandemic also introduced new variables, including increased telehealth utilization and the long-term health implications for survivors, which could have ripple effects on future healthcare spending.

Inflation and Economic Growth

General inflation impacts the cost of everything, including medical services, labor for healthcare providers, and administrative expenses. A period of sustained high inflation, as seen in recent years, can accelerate the rate at which Medicare’s costs grow. Conversely, economic growth can influence wage levels and tax revenues, which contribute to Medicare’s funding. The balance between these economic forces directly affects the financial health of the Medicare program and its ability to absorb costs without significant premium increases.

Legislative and Policy Debates

Medicare is a frequently discussed topic in political discourse. Debates around drug pricing reform, expanding Medicare benefits, or adjusting eligibility criteria can all have profound impacts on the program’s financial structure. Any major legislative changes enacted in the coming years could alter the trajectory of Medicare Part B Premiums. Beneficiaries should stay attuned to policy discussions that could influence their future healthcare costs.

Physician Payment Updates

A significant portion of Part B expenditures goes towards physician services. Annual updates to the Medicare physician fee schedule can influence the overall cost of services. If these payments increase substantially, it can contribute to a rise in Part B premiums. These updates are often a point of contention between healthcare providers and policymakers, balancing adequate compensation for doctors with containing program costs.

Staying Informed and Preparing for 2026

The best defense against unexpected increases in Medicare Part B Premiums is to stay informed and plan ahead. Here’s a checklist to help you prepare:

- Monitor Official Announcements: Keep an eye on announcements from the Centers for Medicare & Medicaid Services (CMS) and the Social Security Administration (SSA) in the fall of 2025. These agencies will release the official premium amounts and IRMAA thresholds for 2026.

- Review Your Income: Understand your Modified Adjusted Gross Income (MAGI) from your 2024 tax return. This will be the basis for your 2026 IRMAA determination. If you anticipate a significant income change for 2025, consider how that might affect 2027 premiums.

- Evaluate Your Coverage Annually: The Annual Enrollment Period (AEP), which runs from October 15th to December 7th each year, is your opportunity to review and change your Medicare coverage. This is the time to compare Medicare Advantage plans, Medigap policies, and Part D prescription drug plans to ensure they still meet your health and financial needs for the upcoming year.

- Understand Your ‘Hold Harmless’ Status: If you receive Social Security benefits, understand whether the ‘hold harmless’ provision applies to you. This provision generally prevents your Part B premium increase from exceeding your Social Security cost-of-living adjustment (COLA). However, it does not apply to those subject to IRMAA, new beneficiaries, or those who don’t have their Part B premiums deducted from Social Security.

- Seek Guidance: Don’t hesitate to reach out to trusted resources. Medicare.gov, the State Health Insurance Assistance Program (SHIP), and qualified financial advisors can provide invaluable assistance in navigating these complex decisions.

By taking these steps, you can ensure that you are well-prepared for any adjustments to Medicare Part B Premiums in 2026, allowing you to maintain access to essential healthcare services without undue financial strain.

Conclusion: Proactive Planning is Key for 2026

The landscape of Medicare is constantly evolving, and understanding the potential changes to Medicare Part B Premiums for 2026 is a critical step in effective retirement planning. While the final figures are yet to be announced, historical trends, economic indicators, and the structure of IRMAA strongly suggest that beneficiaries should anticipate a moderate increase.

The good news is that with proactive planning and informed decision-making, you can mitigate the financial impact of these changes. By strategically managing your income to potentially reduce IRMAA, exploring various Medicare plan options (Original Medicare with Medigap, or Medicare Advantage), and diligently reviewing your coverage annually, you can ensure your healthcare needs remain met without compromising your financial well-being.

Remember, Medicare is a dynamic program, and staying engaged with official announcements and seeking expert advice are your best tools for navigating its complexities. As 2026 approaches, empower yourself with knowledge and make informed choices to secure your healthcare future.