Inflation-Proofing Your Savings: Top Financial Instruments for 2026

In an ever-evolving economic landscape, the specter of inflation consistently looms, threatening to erode the purchasing power of hard-earned savings. For many, ensuring their financial future means not just saving, but actively seeking ways to make those savings resilient against rising costs. As we approach 2026, the imperative to discover effective strategies for inflation-proof savings has never been more critical. This comprehensive guide delves into the top financial instruments designed to safeguard your wealth, providing an average target return of 4.5% or more, allowing your money to not only keep pace with inflation but also grow.

Understanding inflation is the first step towards combating it. Inflation refers to the rate at which the general level of prices for goods and services is rising, and consequently, the purchasing power of currency is falling. If your savings are earning less than the inflation rate, you’re effectively losing money. Therefore, the goal is to identify investments that offer returns exceeding inflation, providing a real return on your capital. This article will explore three robust financial instruments: Treasury Inflation-Protected Securities (TIPS), Real Estate Investment Trusts (REITs), and Dividend-Paying Stocks, detailing how each can contribute to your strategy for inflation-proof savings.

The Silent Threat: Why Inflation Matters for Your Savings

Before diving into specific instruments, it’s crucial to grasp the profound impact inflation has on your financial well-being. Imagine you have $10,000 in a savings account earning a meager 0.5% interest, while inflation is running at 3%. In real terms, your $10,000 is losing 2.5% of its purchasing power each year. Over time, this erosion can significantly diminish your financial security, making it harder to achieve long-term goals like retirement, education, or a down payment on a home. This is why proactive measures for inflation-proof savings are not merely advisable but essential.

The current economic climate, marked by geopolitical tensions, supply chain disruptions, and shifting monetary policies, suggests that inflation could remain a significant concern for the foreseeable future. Historical data consistently shows periods of elevated inflation, underscoring the need for a resilient investment strategy. Relying solely on traditional savings accounts or low-yielding bonds can be detrimental to your financial health in such an environment. The objective is to find investments that either directly adjust for inflation or possess characteristics that allow them to outperform it.

Furthermore, the psychological impact of inflation can be just as damaging. Watching your savings dwindle in real terms can create anxiety and uncertainty about the future. By implementing a sound strategy for inflation-proof savings, you not only protect your wealth but also gain peace of mind, knowing that your financial future is more secure. This article will guide you through instruments that have historically performed well during inflationary periods, offering a path to preserving and growing your capital.

Treasury Inflation-Protected Securities (TIPS): A Direct Hedge Against Inflation

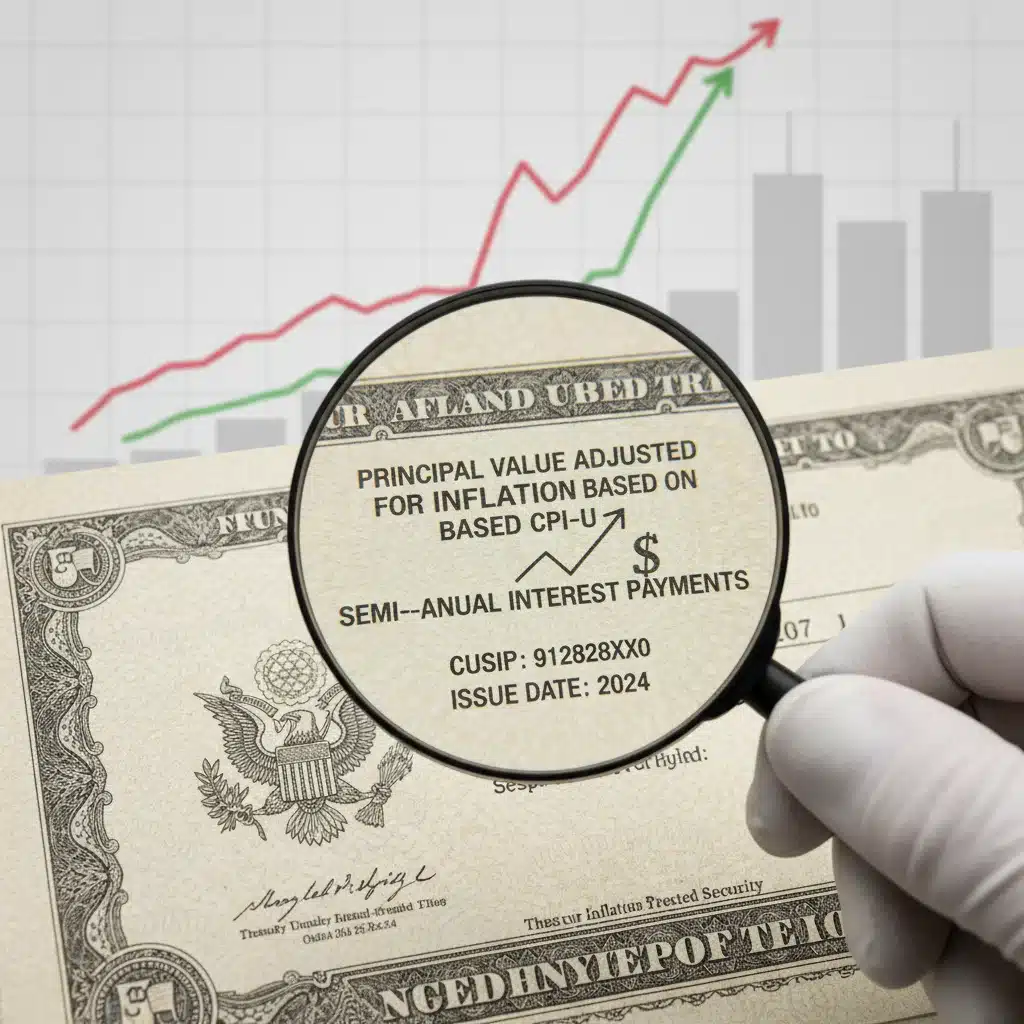

One of the most straightforward and effective ways to achieve inflation-proof savings is through Treasury Inflation-Protected Securities, commonly known as TIPS. These are U.S. Treasury bonds that are indexed to inflation to protect investors from a decrease in the purchasing power of their money. The principal value of a TIPS increases with inflation and decreases with deflation, as measured by the Consumer Price Index (CPI). When a TIPS matures, you receive either the original or adjusted principal, whichever is greater.

Here’s how TIPS work: The principal value of a TIPS adjusts semi-annually based on changes in the CPI. For instance, if the CPI rises, the principal value of your TIPS increases. This increased principal is then used to calculate the interest payments you receive, which are paid semi-annually at a fixed rate. This means both your principal and interest payments grow with inflation, providing a powerful hedge against rising prices. This direct linkage to inflation makes TIPS an excellent component of any strategy aimed at inflation-proof savings.

Let’s consider an example: You invest $10,000 in a TIPS with a fixed interest rate of 1%. If inflation over six months is 2%, your principal will increase to $10,200. Your next interest payment will then be calculated on this new principal, meaning you receive 1% of $10,200, or $102, instead of $100. This mechanism ensures that your investment not only preserves its real value but also generates real returns. While the fixed interest rate might seem modest, the inflation adjustment to the principal is the key to its protective power.

Advantages of TIPS for Inflation-Proof Savings:

- Direct Inflation Protection: The principal value adjusts directly with inflation, preserving your purchasing power.

- Government Backing: TIPS are backed by the full faith and credit of the U.S. government, making them virtually risk-free in terms of default.

- Real Return: Even with low fixed rates, the inflation adjustment ensures a real return on your investment.

- Liquidity: TIPS can be bought and sold on the secondary market before maturity.

Considerations for TIPS:

- Deflation Risk: While principal is protected against deflation at maturity (you receive at least the original principal), interest payments would be calculated on a reduced principal during periods of deflation.

- Interest Rate Risk: Like other bonds, TIPS values can fluctuate with changes in real interest rates. If real rates rise, the market value of existing TIPS may fall.

- Taxation: The increase in principal due to inflation adjustments is taxable in the year it occurs, even though you don’t receive the money until maturity. This is known as “phantom income” and should be considered, especially for investments held in taxable accounts.

Despite these considerations, TIPS remain a cornerstone for investors seeking reliable inflation-proof savings, particularly for those with a long-term horizon and a desire for capital preservation. They are an essential tool in a diversified portfolio, providing a foundational layer of protection against the erosive effects of inflation.

Real Estate Investment Trusts (REITs): Tangible Assets for Growing Wealth

Another powerful instrument for achieving inflation-proof savings, especially with an average target return of 4.5% or more, is Real Estate Investment Trusts (REITs). REITs are companies that own, operate, or finance income-producing real estate across a range of property sectors. They are often compared to mutual funds, but for real estate, allowing individual investors to earn dividends from real estate investments without having to buy, manage, or finance property themselves.

The appeal of REITs in an inflationary environment stems from several factors. Firstly, real estate, as a tangible asset, tends to appreciate in value during periods of inflation. As the cost of building materials and labor rises, new construction becomes more expensive, increasing the value of existing properties. This intrinsic link to inflation helps REITs maintain and grow their asset base, contributing to their ability to provide inflation-proof savings.

Secondly, REITs often generate income through rental payments, which can be adjusted upwards to reflect rising costs and market demand. Lease agreements often include clauses that allow for periodic rent increases, sometimes tied directly to inflation indexes. This ability to pass on increased costs to tenants helps REITs maintain strong revenue streams, which in turn supports their dividend payments to investors. By law, REITs are required to distribute at least 90% of their taxable income to shareholders annually in the form of dividends, making them attractive for income-focused investors.

Consider a diversified REIT portfolio that includes residential, commercial, and industrial properties. As inflation drives up housing costs, residential REITs can increase rents. Similarly, commercial and industrial REITs can adjust lease terms for businesses, ensuring their income keeps pace with economic changes. This diverse exposure to various real estate sectors can offer a robust defense against inflation, enhancing your strategy for inflation-proof savings.

Advantages of REITs for Inflation-Proof Savings:

- Inflation Hedge: Real estate values and rental income tend to rise with inflation, preserving purchasing power.

- High Dividend Yields: The requirement to distribute 90% of taxable income often leads to attractive dividend payouts.

- Diversification: REITs offer portfolio diversification by providing exposure to real estate without direct property ownership.

- Liquidity: Unlike direct real estate ownership, REIT shares are traded on major stock exchanges, offering greater liquidity.

Considerations for REITs:

- Interest Rate Sensitivity: REITs can be sensitive to interest rate changes. Rising interest rates can increase borrowing costs for REITs and make their dividend yields less attractive compared to bonds.

- Market Risk: Like all stocks, REIT prices can fluctuate with overall market conditions and investor sentiment.

- Property-Specific Risks: Performance can be affected by specific real estate market conditions, such as oversupply or regional economic downturns.

For investors seeking a balance of growth, income, and inflation protection, REITs present a compelling option. Their inherent link to tangible assets and ability to adjust income streams make them a valuable asset in constructing a portfolio geared towards inflation-proof savings.

Dividend-Paying Stocks: Growth and Income in an Inflationary Environment

The third pillar for building inflation-proof savings is investing in high-quality dividend-paying stocks, particularly those from companies with strong pricing power and a history of increasing dividends. While not a direct hedge like TIPS, certain dividend stocks can outperform inflation by growing their earnings and, consequently, their dividends at a rate that exceeds the cost of living.

Companies with strong pricing power operate in industries where they can raise the prices of their goods and services without significantly impacting demand. These are often established companies with dominant market positions, strong brand loyalty, or essential products/services. As inflation drives up their input costs, they can pass those costs onto consumers, thereby protecting their profit margins. This ability to maintain profitability is crucial for sustaining and growing dividend payments, making them excellent candidates for inflation-proof savings.

Furthermore, companies that consistently increase their dividends over time are often referred to as “dividend aristocrats” or “dividend champions.” These are businesses with robust financial health, stable cash flows, and a commitment to returning value to shareholders. The growth in their dividends can often outpace inflation, providing investors with a rising income stream that helps maintain purchasing power. This dual benefit of capital appreciation potential and growing income makes dividend stocks a powerful tool in your inflation-fighting arsenal.

Consider investing in companies that produce essential goods, utilities, or consumer staples. These sectors tend to be more resilient during economic downturns and inflationary periods because demand for their products and services remains relatively stable. For example, a utility company might have regulated rate increases that account for inflation, ensuring consistent revenue growth. A consumer staples company might have strong brand loyalty that allows it to incrementally raise prices without losing market share. These characteristics are vital for selecting dividend stocks that contribute to inflation-proof savings.

Advantages of Dividend-Paying Stocks for Inflation-Proof Savings:

- Capital Appreciation: Beyond dividends, these stocks offer the potential for their share price to grow, driven by company performance and market demand.

- Growing Income Stream: Companies with a history of increasing dividends can provide an income stream that grows faster than inflation.

- Business Growth: Investing in strong companies means participating in their growth and profitability.

- Diversification: A diversified portfolio of dividend stocks across various sectors can provide broad market exposure and reduce risk.

Considerations for Dividend-Paying Stocks:

- Market Volatility: Stock prices can be volatile, and even fundamentally strong companies can experience price declines.

- Dividend Cuts: While rare for established dividend payers, companies can cut or suspend dividends during challenging economic times.

- Sector-Specific Risks: Performance can be tied to the specific industry or sector the company operates in.

For investors willing to undertake a degree of market risk in exchange for potential growth and a rising income stream, dividend-paying stocks are an indispensable component of an effective strategy for inflation-proof savings. Careful selection of companies with strong fundamentals and a track record of dividend growth is key to success.

Building a Diversified Portfolio for Inflation-Proof Savings

While each of these instruments – TIPS, REITs, and Dividend-Paying Stocks – offers unique benefits for combating inflation, the most effective strategy for inflation-proof savings involves a diversified approach. Combining these assets within a single portfolio can help mitigate the individual risks associated with each while maximizing the overall protection against inflation.

Diversification is not just about spreading your money across different asset classes; it’s also about combining assets that behave differently under various economic conditions. For instance, while TIPS offer direct inflation protection, their returns might be lower during periods of disinflation. REITs offer capital appreciation and income linked to real estate, but they can be sensitive to interest rate hikes. Dividend stocks provide growth and rising income but carry equity market risk.

A balanced portfolio might allocate a portion of funds to TIPS for foundational inflation protection and principal preservation. Another portion could go into REITs to capture the benefits of real estate appreciation and rental income. Finally, a selection of high-quality dividend-paying stocks could add growth potential and a resilient income stream. This synergistic approach creates a more robust defense against inflation, allowing your wealth to not only be preserved but also to grow at a target average return of 4.5% or more over the long term.

Key Principles for Diversification:

- Asset Allocation: Determine the appropriate mix of TIPS, REITs, and dividend stocks based on your risk tolerance, time horizon, and financial goals.

- Regular Rebalancing: Periodically review and adjust your portfolio to maintain your desired asset allocation.

- Continuous Research: Stay informed about economic trends and the performance of your chosen investments.

Remember, the goal is not just to beat inflation in a single year but to build a sustainable strategy that ensures your inflation-proof savings for years to come. This requires a thoughtful approach to investment selection and ongoing management.

Beyond the Instruments: Other Considerations for Inflation-Proof Savings

While the focus has been on specific financial instruments, several other factors contribute to a comprehensive strategy for inflation-proof savings. These include personal financial habits, understanding economic indicators, and seeking professional advice.

Personal Financial Habits:

- Budgeting and Expense Management: Keeping your personal expenses in check can free up more capital for investments that combat inflation.

- Emergency Fund: Maintain a robust emergency fund in a high-yield savings account or short-term TIPS to cover unexpected expenses without liquidating longer-term investments.

- Debt Management: High-interest debt can be particularly burdensome during inflationary periods. Prioritize paying off consumer debt to free up cash flow.

Understanding Economic Indicators:

- Consumer Price Index (CPI): Keep an eye on CPI reports to understand current inflation trends.

- Interest Rates: Monitor central bank policies and interest rate movements, as they can impact bond yields and the attractiveness of income-generating assets.

- Economic Growth: Strong economic growth can support corporate earnings and real estate values, but too much growth can also fuel inflation.

Seeking Professional Advice:

Navigating the complexities of investment markets, especially with the goal of inflation-proof savings, can be challenging. A qualified financial advisor can help you assess your personal financial situation, define your goals, and construct a personalized investment plan that aligns with your risk tolerance and inflation concerns. They can provide insights into specific investment products, tax implications, and help you rebalance your portfolio as economic conditions change.

Conclusion: Securing Your Financial Future Against Inflation

The journey to achieving inflation-proof savings is an ongoing process that requires vigilance, strategic planning, and a diversified investment approach. As we look towards 2026, the instruments discussed – Treasury Inflation-Protected Securities (TIPS), Real Estate Investment Trusts (REITs), and Dividend-Paying Stocks – offer compelling avenues to protect and grow your wealth in the face of rising costs. Each instrument brings unique strengths to the table, and when combined thoughtfully, they form a formidable defense against the erosion of purchasing power.

By understanding the mechanisms of TIPS, leveraging the tangible asset backing of REITs, and harnessing the growth and income potential of robust dividend stocks, investors can build a resilient portfolio designed to outperform inflation, aiming for that desirable average return of 4.5% or more. Remember that diversification, regular review, and continuous education are paramount to long-term success. Don’t let inflation silently diminish your hard work. Take proactive steps today to secure a brighter, more financially stable future.

Investing in your financial education and making informed decisions are the best ways to ensure your savings are not just preserved, but truly inflation-proof savings. Begin your journey today by exploring these powerful financial instruments and consulting with financial professionals to tailor a strategy that best suits your individual needs and aspirations.